An Unexpected Dip for My Credit Score: FICO Score Now at 753

Two weeks ago, I logged into my Citibank consumer credit card account -- the only consumer credit card account I have with a balance right now -- to find that the good folks at Citi had recently given me a credit line increase, and a substantial one at that. My credit limit was around $13,000; now it's close to $22,000. 22K is the highest credit limit I've ever been granted. Not even my strongest business credit card has a credit limit that high.

Of course, I was very pleased about the credit increase, because it means that the balance on this particular card is now a smaller fraction of the account's credit limit, and that looks good to my current and potential creditors.

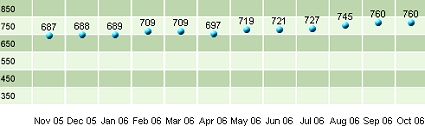

Funny thing is, my FICO® credit score (provided by Transunion), which had been hovering at 760 for the past two months, has dropped to 753. Now, I realize that the best way to get my FICO score to rise is to pay down my consumer credit card debt: the bigger the payment, the bigger the bump to my score. But since the balance on my Citi consumer credit card is now close to a third of my total credit line, my thinking was this would cause at least a small increase for my score.

Unexpected Decline for My Credit Score: Must Be Identity Theft!

Since I was expecting a small rise for my FICO score this month, as soon as I noticed the lower score, my immediate reaction was to order a free credit report from each of the 3 credit bureaus. I had to rule out the possibility that someone had gained my sensitive info and used it to open one or more accounts in my name. Under federal law, you are entitled to one free copy of your credit report (also known as a "credit file disclosure") every year from the 3 majors -- Transunion, Experian and Equifax. I had never exercised my right to a free report, so it seemed like the perfect time to take advantage of the new law.

I stopped by the www.Annualcreditreport.com website to order my free reports (Congress mandated that the 3 bureaus create the Annualcreditreport.com website. It's the site you need to use to get your free annual credit report from the 3 majors, or you can call 877-322-8228. If you contact any of the credit bureaus directly, you'll probably be asked to pay a fee.) After bypassing all the extra stuff the credit bureaus tried to sell me, I was able to get a free copy of my report from each agency quite quickly. I reviewed all the data carefully, and found nothing out of order.

Was I being paranoid for assuming that someone had stolen my identity? I don't think so! And here's why: Last month, I performed a virus scan on all my computers and the virus scanner found a keylogger installed on my primary workstation. A keylogger! I was floored by the discovery. With all the precautions I take -- virus scanner, firewall, etc. -- someone was still able to get a keylogger program installed on my computer. Unbelievable. I am not going to do the idiots who create these programs any favors by posting the name of the trojan here, but I will share this: the trojan almost succeeded at collecting many of my usernames and passwords -- and the corresponding website URL's! Had the trojan succeeded, it would have sent my many credentials to the criminals who probably know exactly how to exploit them for maximum gain, or maximum damage.

So remember to run a virus scan regularly, and remember to keep your virus definition files up to date!

A Downgraded Credit Score: It Feels Like I Failed A College Midterm.

So, why did my FICO score regress? I haven't opened any new accounts, or performed any balance transfers lately. For all my personal spending, it's been all cash (or debit card) for some time now. My understanding was that as your accounts age and you pay down your balances, you score goes up. Maybe the scoring algorithm was recently modified in some way. Maybe it was a simple correction. Whatever the reason, the decline in my score has certainly rubbed me wrong, and I plan on making a $900+ payment to my Citibank consumer credit card next week, which I'm hoping will boost my FICO score above 770. Wish me luck!

Always Negotiate -- Even Your Rent!

I do have some good news to report. I recently renewed the lease for my apartment and was able to get a favorable deal. The folks who manage my apartment complex wanted to raise my rent by $250 per month. I realize that a rent increase is quite normal for a place like mine, but $250 was simply not reasonable. I met with the property manager and negotiated (I brought my baby girl along to the negotiating table; gotta' use all the tools God gave me!) In the end, the property manager agreed to raise my rent by $20, which I calculated to be considerably lower than the rate on inflation, so I was OK with it. It's like Frederick Douglass said, "Power cedes nothing without a demand."

Here's an updated image of my charted credit score:

Of course, I was very pleased about the credit increase, because it means that the balance on this particular card is now a smaller fraction of the account's credit limit, and that looks good to my current and potential creditors.

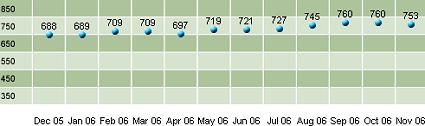

Funny thing is, my FICO® credit score (provided by Transunion), which had been hovering at 760 for the past two months, has dropped to 753. Now, I realize that the best way to get my FICO score to rise is to pay down my consumer credit card debt: the bigger the payment, the bigger the bump to my score. But since the balance on my Citi consumer credit card is now close to a third of my total credit line, my thinking was this would cause at least a small increase for my score.

Unexpected Decline for My Credit Score: Must Be Identity Theft!

Since I was expecting a small rise for my FICO score this month, as soon as I noticed the lower score, my immediate reaction was to order a free credit report from each of the 3 credit bureaus. I had to rule out the possibility that someone had gained my sensitive info and used it to open one or more accounts in my name. Under federal law, you are entitled to one free copy of your credit report (also known as a "credit file disclosure") every year from the 3 majors -- Transunion, Experian and Equifax. I had never exercised my right to a free report, so it seemed like the perfect time to take advantage of the new law.

I stopped by the www.Annualcreditreport.com website to order my free reports (Congress mandated that the 3 bureaus create the Annualcreditreport.com website. It's the site you need to use to get your free annual credit report from the 3 majors, or you can call 877-322-8228. If you contact any of the credit bureaus directly, you'll probably be asked to pay a fee.) After bypassing all the extra stuff the credit bureaus tried to sell me, I was able to get a free copy of my report from each agency quite quickly. I reviewed all the data carefully, and found nothing out of order.

Was I being paranoid for assuming that someone had stolen my identity? I don't think so! And here's why: Last month, I performed a virus scan on all my computers and the virus scanner found a keylogger installed on my primary workstation. A keylogger! I was floored by the discovery. With all the precautions I take -- virus scanner, firewall, etc. -- someone was still able to get a keylogger program installed on my computer. Unbelievable. I am not going to do the idiots who create these programs any favors by posting the name of the trojan here, but I will share this: the trojan almost succeeded at collecting many of my usernames and passwords -- and the corresponding website URL's! Had the trojan succeeded, it would have sent my many credentials to the criminals who probably know exactly how to exploit them for maximum gain, or maximum damage.

So remember to run a virus scan regularly, and remember to keep your virus definition files up to date!

A Downgraded Credit Score: It Feels Like I Failed A College Midterm.

So, why did my FICO score regress? I haven't opened any new accounts, or performed any balance transfers lately. For all my personal spending, it's been all cash (or debit card) for some time now. My understanding was that as your accounts age and you pay down your balances, you score goes up. Maybe the scoring algorithm was recently modified in some way. Maybe it was a simple correction. Whatever the reason, the decline in my score has certainly rubbed me wrong, and I plan on making a $900+ payment to my Citibank consumer credit card next week, which I'm hoping will boost my FICO score above 770. Wish me luck!

Always Negotiate -- Even Your Rent!

I do have some good news to report. I recently renewed the lease for my apartment and was able to get a favorable deal. The folks who manage my apartment complex wanted to raise my rent by $250 per month. I realize that a rent increase is quite normal for a place like mine, but $250 was simply not reasonable. I met with the property manager and negotiated (I brought my baby girl along to the negotiating table; gotta' use all the tools God gave me!) In the end, the property manager agreed to raise my rent by $20, which I calculated to be considerably lower than the rate on inflation, so I was OK with it. It's like Frederick Douglass said, "Power cedes nothing without a demand."

Here's an updated image of my charted credit score:

Labels: 753, credit_score, fico, negotiate, rent, transunion

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by FedPrimeRate.com | 11/24/2006 06:12:00 PM

|

0 comments

links to this post

![]()

![]()