Losing Track of Student Loans Can Wreak Havoc On Your Personal Finances

While having a big family is a wonderful blessing in and of itself, it’s especially rewarding during tax season. Don’t get me wrong; I value my family infinitely more than a tax refund, but it feels good to know that my commitment to my marriage and children is recognized by our government when tax time rolls around. We had twins last year, so when my husband and I realized that we would get a Child Tax Credit for both of them, we thought that was pretty nice. After deductions, we expected a return in the thousands, so we were happy campers.

While having a big family is a wonderful blessing in and of itself, it’s especially rewarding during tax season. Don’t get me wrong; I value my family infinitely more than a tax refund, but it feels good to know that my commitment to my marriage and children is recognized by our government when tax time rolls around. We had twins last year, so when my husband and I realized that we would get a Child Tax Credit for both of them, we thought that was pretty nice. After deductions, we expected a return in the thousands, so we were happy campers.During that same time, however, we were dealing with a frustrating issue that did not put smiles on our faces at all. Somehow, when I consolidated my federal student loans, one of them was not included. I didn’t understand how it could have happened, considering how informed the consolidation company was. Loan consolidators do all of the hard work for you - they call you out of the blue, offering to make your life easier by combining your student loans with a great interest rate and anything else you need, including forbearances. As they are explaining everything to you at the speed of light, they list all of your outstanding loans and help you to understand why making one easy monthly payment would ease your anxieties about student loan debt. They’re right; it does. So, I agreed with them and consolidated my loans. They reviewed the information with me again, reading back the information on each smaller loan that would be merged together into the big loan. So, I thought everything was taken care of.

And then we found the one that got away.

Actually, the one that got away found us; once the creditor discovered I had moved and gotten married, they politely called to let me know that I owed them money for a small student loan. It took a while to figure out what happened, but when we did, my heart sank. I was so young and I took out so many small loans while I was in school that I hadn’t been keeping track of them properly. So, when the consolidators did not have their facts and figures right, I should have been able to correct them, but I wasn‘t. I ended up with a defaulted loan because it went unpaid and unnoticed for quite some time. As many young Americans know, having a student loan in default is guaranteed to bring a lot of unwanted phone calls, anxiety, and grief that we did not want. One artist was so encumbered by Sallie Mae that he wrote a song about it:

So, we did everything we had to do to bring that loan back to current status, although it didn't happen until around the time we filed our taxes for the year. Thinking that everything was settled, we filed and waited, only to learn that the creditor had not reported the updated status of the loan, so our entire federal refund would be garnished to settle the debt.

Needless to say, that knocked the wind out of my sail.

Lots of people depend on their federal tax returns each year to cover large expenses or to revive their personal finances. However, outstanding student loans, if they are not current or at least in forbearance, can cause your federal income tax refund to be garnished. Although what we lost was actually enough to pay off the debt and would release us from it, we couldn‘t help but feel blindsided. Our tax preparer told us that we could have appealed the situation, considering that the return was garnished unnecessarily. We decided to just let it go. Although we mourned the loss of our beloved tax return, debt freedom, much like family, is simply too great a commitment to take lightly.

Labels: debt_freedom, default, I_C_Jackson, settling debt, student_loan_debt, tax_refund, tax_season

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by I.C. Jackson | 9/27/2008 09:04:00 AM

|

0 comments

links to this post

![]()

![]()

My next idea was to take advantage of one of the 0% balance transfer checks that I often receive via snail mail, offers from credit card companies with which I already have an account. In fact, today I got one from Bank of America, and it fit the bill nicely. The balance on my student loan debt is a little over $11,500 (I called for a payoff quote), and this particular Bank of America account has a credit limit that's close to $13,000. All I would have had to do was sign the check, mail it to ED, and the debt would have been transferred to my card. I would have paid no interest on the debt until January 2009. I wouldn't have waited that long to pay it down to zero, however; I would have paid the card off within 4 to 5 months.

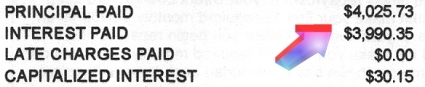

My next idea was to take advantage of one of the 0% balance transfer checks that I often receive via snail mail, offers from credit card companies with which I already have an account. In fact, today I got one from Bank of America, and it fit the bill nicely. The balance on my student loan debt is a little over $11,500 (I called for a payoff quote), and this particular Bank of America account has a credit limit that's close to $13,000. All I would have had to do was sign the check, mail it to ED, and the debt would have been transferred to my card. I would have paid no interest on the debt until January 2009. I wouldn't have waited that long to pay it down to zero, however; I would have paid the card off within 4 to 5 months. So, last Wednesday, I logged onto the Capital One website to get a payoff quote for my auto loan. On Thursday morning, I visited my local post office and mailed, via overnight express, a check for a tad over $9,000. Today, I was able to login to the Capital One site and confirm that the payment was received. Yahoo. Feels pretty good: I own a great car, and I no longer have car payments (I was paying around $349 per month.)

So, last Wednesday, I logged onto the Capital One website to get a payoff quote for my auto loan. On Thursday morning, I visited my local post office and mailed, via overnight express, a check for a tad over $9,000. Today, I was able to login to the Capital One site and confirm that the payment was received. Yahoo. Feels pretty good: I own a great car, and I no longer have car payments (I was paying around $349 per month.)